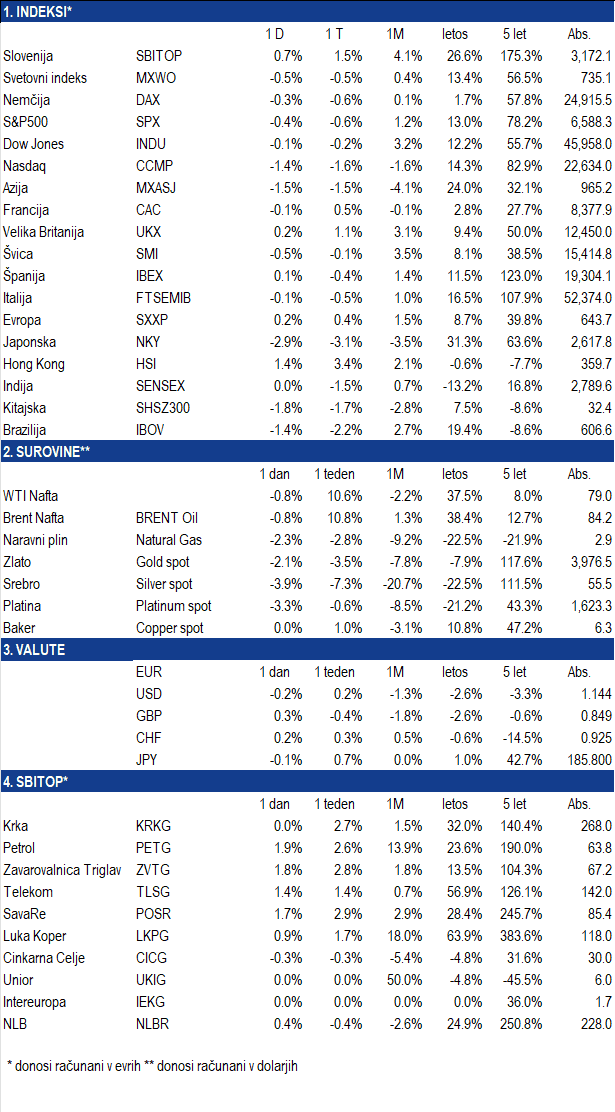

News

News and insights.

Market commentaries, ILIRIKA news, and insights from our experts — everything to help you stay up to date with the investment world.

V tem tednu:

Delničarji Addiko Bank, ki so že sprejeli konkurenčno ponudbo, jo lahko prekličejo do 23. julija 2026 in svoje delnice vključijo v NLB-jevo prevzemno ponudbo. NLB je podaljšala prevzemno ponudbo za Addiko Bank, prevzemni prag znižala na 50 odstotkov plus eno delnico ter ponudila 37 evrov za delnico, kar predstavlja 39,6 odstotka višjo ponudbo od konkurenčne ponudbe RBI.

Krka dosegla novo rekordno vrednost delnice ter v Novem mestu odprla nov večnamenski objekt s centralno kuhinjo za oskrbo 11 restavracij v svojih slovenskih obratih.

Triglav vstopa v hrvaško zasebno zdravstvo z nakupom 49-odstotnega deleža skupine Arsano Medical Group.

Irma Gubanec imenovana za podpredsednico uprave Telekoma Slovenije; štiriletni mandat začne oktobra.

Ameriška inflacija in proizvajalske cene so se junija dodatno umirile, kar je okrepilo pričakovanja o znižanju obrestnih mer Fed.

Trge zaznamujejo različni odzivi centralnih bank na inflacijo, višje obrestne mere in geopolitična tveganja: ECB zaostruje politiko zaradi dražje energije, vlagatelji spremljajo ameriške in britanske odločitve, negotovost pa povečujejo razmere v Hormuški ožini; kljub temu ostajajo pomembni kakovost podjetij, zmerna vrednotenja in prihajajoči poslovni rezultati, med katerimi izstopa Krka z rastjo prihodkov (+7 %), dobička (+5 %) in višjo dividendo (9,10 evra na delnico).

JPMorgan Chase je z boljšimi rezultati od pričakovanj uspešno odprl sezono objav poslovnih rezultatov ameriških bank.

TSMC je zaradi močnega povpraševanja po čipih za umetno inteligenco povečal četrtletni dobiček za 77 odstotkov.

V prihodnjem tednu:

Četrtletna poročila: Alphabet, Novartis, Intel, Philip Morris, Nestle, T-Mobile, SAP, UniCredit, Volkswagen.

Makroekonomski kazalci: Evropa – PMI indeks, obrestna mera ECB za mejni depozit in za operacije glavnega refinanciranja; ZDA – PMI indeks.

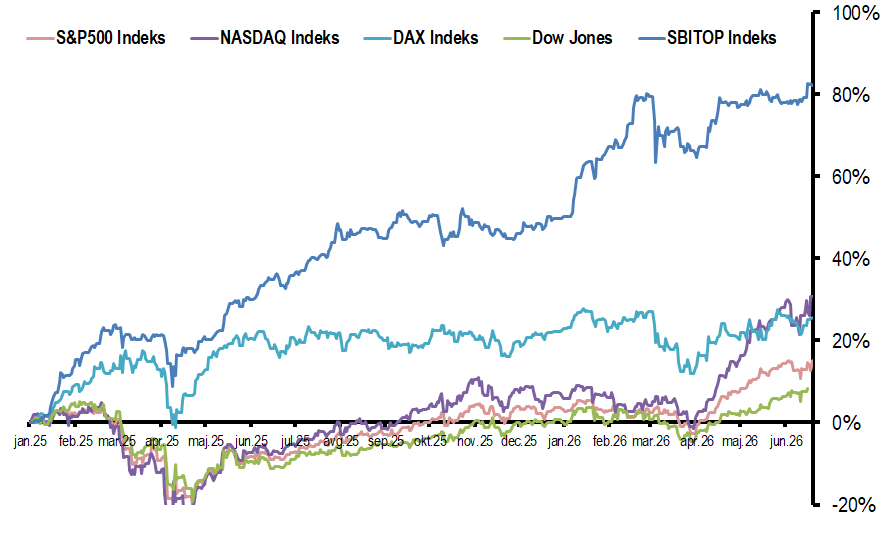

Gibanje indeksov

Vir: Bloomberg

Slovenski delniški trg nadaljuje zelo uspešno leto. Indeks SBITOP je od začetka leta pridobil okoli 22 odstotkov, julija pa je dosegel novo rekordno vrednost nad 3.180 točkami. Rast je široko razpršena. Najbolj izstopata Luka Koper in Telekom Slovenije, močno pa so pridobile tudi Krka, Sava Re, NLB, Petrol in Zavarovalnica Triglav.

Slovenski trg je kljub rasti še vedno cenejši od večine razvitih tujih trgov. Indeks SBITOP se vrednoti pri približno 14-kratniku pričakovanega dobička, ob tem pa ponuja okoli 3,6-odstotno dividendno donosnost. Visoka dobičkonosnost družb, močne bilance in radodarne dividendne politike tako še naprej podpirajo zanimanje domačih in tujih vlagateljev. Dodatno zanimanje spodbuja začetek trgovanja z ETF SLOTR, ki omogoča enostavno in razpršeno izpostavljenost do vodilnih slovenskih borznih družb. Primeren je tako za individualne naložbene in trgovalne račune kot tudi za institucionalne vlagatelje.

Kako lahko borza podpre rast in prevzeme, kaže tudi hrvaški Bosqar, ki je z izdajo novih delnic zbral 150 milijonov evrov, povpraševanje pa je preseglo ponudbo. Kapital bo namenjen nadaljnji regionalni širitvi in razvoju prehranske platforme, v kateri je tudi slovenska Panvita. Pomembno vlogo pri razvoju hrvaškega kapitalskega trga ima obvezni drugi pokojninski steber, ki zagotavlja stabilnejšo bazo dolgoročnega domačega povpraševanja.

Tudi Slovenija ima več kot 30 milijard evrov bančnih vlog ter pomemben kapital gospodinjstev, podjetij, pokojninskih skladov in zavarovalnic. Ob generacijskem prehodu bi bilo zato smiselno razvijati nove domače borzne platforme, ki bi kapital lažje usmerjale v rast, povezovanje in lastniške prehode slovenskih podjetij. Takšne rešitve bi lahko ob sodelovanju javnih in zasebnih vlagateljev podprle tudi večje naložbe doma in v regiji.

V ospredju ostaja Krka, katere delnica je ta teden dosegla novo rekordno vrednost 270 evrov. Na skupščini 9. julija je predsednik uprave Jože Colarič predstavil oceno poslovanja za prvo polletje. Prihodki skupine so se povečali za sedem odstotkov na 1,12 milijarde evrov, EBITDA za 18 odstotkov, dobiček iz poslovanja za 20 odstotkov, čisti dobiček pa za pet odstotkov na več kot 260 milijonov evrov. Po navedbah uprave so bili operativni rezultati najboljši od ustanovitve družbe, dosedanje poslovanje pa kaže, da bo Krka dosegla načrtovane celoletne cilje.

Prodaja se je povečala v petih od šestih regij. Največja ostaja vzhodna Evropa, kjer je rast podpirala predvsem 15-odstotna rast prodaje v Rusiji. Najhitreje so rasli čezmorski trgi, medtem ko je prodaja v zahodni Evropi nekoliko upadla.

Skupščina je potrdila izplačilo 9,10 evra bruto dividende na delnico, kar je 10,3 odstotka več kot lani. Do nje bodo upravičeni delničarji, vpisani v delniško knjigo 22. julija, izplačevanje pa se začne 23. julija. Istega dne bo Krka po obravnavi nadzornega sveta objavila tudi nerevidirane rezultate za prvo polletje. Uprava je za 36 mesecev dobila še pooblastilo za nakupe lastnih delnic do desetih odstotkov osnovnega kapitala, omogočen pa je tudi njihov poznejši umik. Družba je v Novem mestu odprla še večnamenski objekt s centralno kuhinjo za oskrbo enajstih restavracij v svojih slovenskih obratih.

Živahno ostaja tudi pri drugih domačih družbah. Zavarovalnica Triglav z nakupom 49-odstotnega deleža skupine Arsano Medical Group vstopa na hrvaški trg zasebnega zdravstva. NLB je podaljšala prevzemno ponudbo za Addiko Bank in prevzemni prag znižala na 50 odstotkov plus eno delnico, s čimer je povečala možnosti za uspešen zaključek prevzema. V Telekomu Slovenije je bila za podpredsednico uprave imenovana Irma Gubanec, ki bo štiriletni mandat začela oktobra.

Po Krki se bo avgusta nadaljevala sezona objav polletnih rezultatov. Poročali bodo NLB, Triglav, Sava Re, Luka Koper, Telekom Slovenije, Petrol, Cinkarna Celje in druge domače družbe. Rezultati bodo pokazali, ali bo močna rast slovenskih delnic dobila nadaljnjo podporo tudi v poslovanju podjetij.

Read more

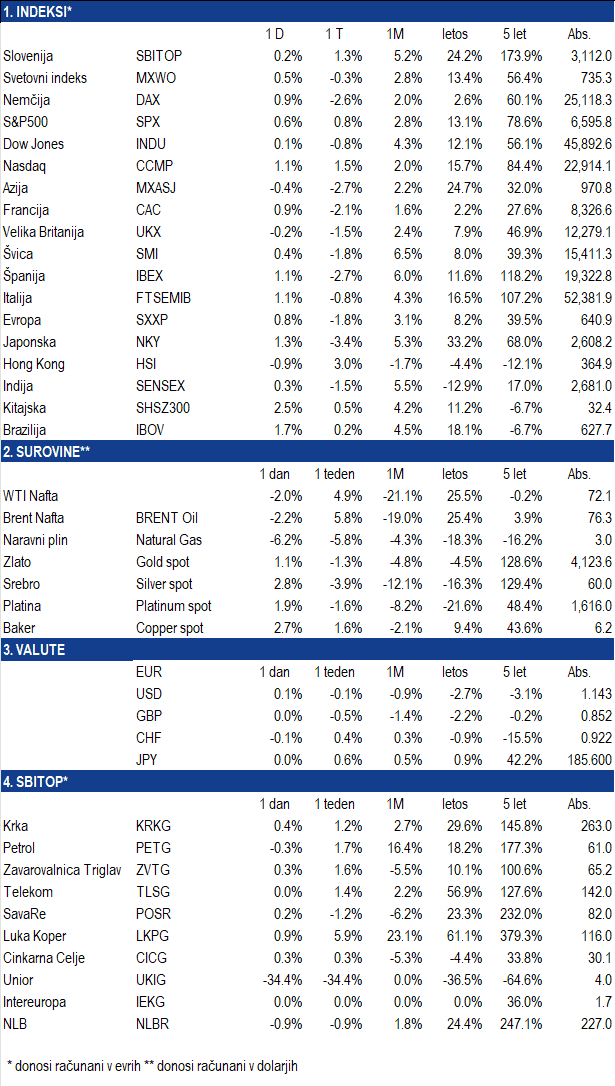

V tem tednu:

Krka je prvo polletje po prvih ocenah zaključila zelo solidno: prihodki od prodaje so zrasli za 7% na 1,14 milijarde evrov, čisti dobiček pa za 5% na 260 milijonov evrov, ob tem pa družba nadaljuje tudi privlačno dividendno politiko z 9,10 evra bruto dividende na delnico, kar je 10,3% več kot lani.

V kratkem bo na Ljubljanski borzi začel trgovati tudi globalni ETF WORLD, ki bo vlagateljem omogočal razpršeno izpostavljenost do razvitih svetovnih trgov in bo primeren za uporabo znotraj individualnih naložbenih računov.

Na Ljubljanski borzi že trguje ETF Slovenija (SLOTR), ki je izredno primeren za individualne naložbene račune, saj vlagatelju z enim samim nakupom omogoča razpršeno izpostavljenost do vodilnih slovenskih borznih družb; zaradi pregledne strukture, nizkih stroškov, borzne likvidnosti in sledenja indeksu SBITOP TR pa je zanimiv tudi za pokojninske sklade, vzajemne sklade, zavarovalnice in druge institucionalne vlagatelje, kot tudi za posameznike in podjetja.

UniCredit želi prevzeti Commerzbank predvsem zaradi ekonomije obsega in velikih stroškovnih sinergij, saj bančništvo postaja vse bolj digitalno in tehnološko, kjer večja banka lažje razporedi stroške IT-sistemov, regulative in razvoja na širšo bazo komitentov; ključna odprta tema pa ostaja, koliko teh prihodnjih sinergij pripada UniCreditu kot učinkovitejšemu upravljavcu in koliko jih bo moral skozi višjo ponudbo deliti z delničarji Commerzbank.

Po spominskih čipih se pozornost vlagateljev v AI dobavni verigi seli tudi na manj opazne, a ključne komponente, kot so MLCC keramični kondenzatorji, ki uravnavajo napetost in stabilnost delovanja AI strežnikov; ker lahko posamezen napreden strežniški sistem potrebuje več sto tisoč takšnih komponent, trg v njih vidi novo možno ozko grlo in vir cenovne moči za največje azijske dobavitelje, kot so Murata, TDK, Taiyo Yuden, Yageo, Walsin in Samsung Electro-Mechanics, medtem ko je med bolj znanimi ameriškimi AI dobavitelji v tej zgodbi še Micron (MU).

Kljub geopolitičnim napetostim, višjim cenam nafte in občasnim skrbem glede potrošnje ostaja razpoloženje na trgih razmeroma stabilno, saj ga podpirajo visoka likvidnost, pričakovana rast dobičkov podjetij, močna AI investicijska zgodba in še vedno solidni makroekonomski podatki; vlagatelji zato tudi ob povečani negotovosti še naprej iščejo priložnosti predvsem v tehnološkem sektorju in širši dobavni verigi umetne inteligence.

V prihodnjem tednu:

Četrtletna poročila: JPM, BoA, Goldman Sachs, Citigroup, Wells Fargo.

Makroekonomski kazalci: Evropa – avkcije državnih obveznic, ZDA – inflacija.

Gibanje indeksov

Vir: Bloomberg

Najboljši portfelj ni tisti, ki ima največ naložb ali najvišji pričakovani donos. Je tisti, ki je izdelan za konkretnega človeka: za izvor njegovega premoženja, obveznosti, življenjsko obdobje, likvidnostne potrebe in tveganja, ki jih pogosto sploh ne vidi. Slovenci imamo na bančnih računih več kot 30 milijard evrov prihrankov. V zadnjih desetih letih je skupna inflacija znašala 31,7 odstotka. Kljub temu velika večina Slovencev še vedno odlaša z vlaganjem v donosnejše naložbe. Razmere se nekoliko izboljšujejo z uvedbo individualnih naložbenih računov, saj je bilo odprtih že več kot 10.000 takšnih računov

Ko ljudje vprašajo, kateri portfelj je najboljši, običajno pričakujejo seznam: koliko delnic, obveznic in zlata. Toda vsi lahko kupijo enake naložbe, ne bi pa smeli imeti enakega portfelja. Dober portfelj zato vsebuje dele, ki se odzivajo na različna okolja. Ob gospodarski rasti lahko delajo delnice. Ko se rast upočasni in padajo obrestne mere, lahko pridobivajo kakovostne obveznice. Ob inflacijskem presenečenju lahko bolje delujejo zlato, surovine…

Podjetnik, ki ima večino premoženja v lastnem podjetju, je že izpostavljen gospodarski rasti, panogi, državi in ključnim strankam. Če prosti denar vloži še v domače banke, industrijo in nepremičnine, je njegov trgovalni račun lahko na videz razpršen, celotno premoženje pa še vedno temelji na enem samem scenariju. Podobno velja za lastnika več nepremičnin. Njegovo premoženje je že povezano z domačim gospodarstvom, obrestnimi merami, regulacijo in lokalno demografijo. Dodatna naložba v nepremičninske družbe tveganja ne zmanjšuje, ampak ga podvaja. Dober portfelj zato ne začne pri vprašanju, kaj kupiti. Začne pri vprašanju, katera tveganja vlagatelj že ima in katera je smiselno še prevzeti.

Več imen še ne pomeni razpršenosti

Razpršenost ni zgolj večje število delnic, ampak število neodvisnih razlogov, zaradi katerih portfelj ustvarja donos. Vlagatelj ima lahko dvajset delnic iz sedmih panog, pa je še vedno odvisen od enega motorja: gospodarske rasti in pripravljenosti vlagateljev na tveganje. Ko pride recesija ali likvidnostni šok, se navidezno različne naložbe začnejo gibati enako. Dober portfelj zato vsebuje dele, ki se odzivajo na različna okolja. Ob gospodarski rasti lahko delajo delnice. Ko se rast upočasni in padajo obrestne mere, lahko pridobivajo kakovostne obveznice. Ob inflacijskem presenečenju lahko bolje delujejo zlato, surovine ali podjetja z močjo oblikovanja cen. V času stresa postaneta dragocena likvidnost in možnost kupovanja takrat, ko morajo drugi prodajati. Namen ni, da vsak del portfelja ves čas raste. Namen je, da celota ni odvisna od enega samega motorja.

Pri večjem premoženju cilj praviloma ni najvišji donos v enem letu. Tak rezultat je najlažje doseči z večjo koncentracijo in večjim tveganjem. Pravi cilj je, da premoženje dolgoročno raste hitreje od inflacije, davkov in porabe, hkrati pa ostane dovolj stabilno in likvidno, da vlagatelju ni treba prodajati ob napačnem času. Po 50-odstotnem padcu je za vrnitev na začetno vrednost potrebna 100-odstotna rast. Pri večjem premoženju je zato pogosto pomembneje preprečiti eno veliko napako kot vsako leto loviti nekaj dodatnih odstotnih točk donosa.

Vrednost je v celoti

Izbrati posamezno delnico je danes lažje kot nekoč. Informacij je ogromno, trgovanje je cenejše, dostop do svetovnih trgov pa skoraj neomejen. Težji del je iz posameznih naložb sestaviti smiselno celoto. Treba je razumeti, kako se naložbe povezujejo z vlagateljevim podjetjem, nepremičninami, prihodki, dolgovi in prihodnjimi obveznostmi. Prepoznati je treba skrite koncentracije, določiti potrebno likvidnost ter zgraditi portfelj, ki ne temelji na eni sami napovedi. Najboljši portfelj zato ni najbolj drzen in ne najbolj zapleten. Je portfelj, v katerem ima vsaka naložba svojo nalogo, vsako tveganje svojo mejo in celota jasen namen.

Premoženje ni le številka na računu. Je varnost družine, svoboda odločanja, možnost naslednje investicije in pogosto rezultat desetletij dela.

Read more

V tem tednu:

Novi ETF SLOTR vlagatelju z enim nakupom omogoča izpostavljenost do vodilnih slovenskih podjetij iz indeksa SBITOP TR. Celotne prejete dividende se samodejno reinvestirajo, zato ostajajo naložene in povečujejo vrednost sklada.

Slovenski delniški trg kljub letošnji rasti ostaja razumno vrednoten. Družbe imajo večinoma močne bilance, nizko zadolženost in stabilne denarne tokove, kar ustvarja dobre temelje za nadaljnjo rast poslovanja ter ohranjanje visokih dividendnih izplačil.

NLB ostaja podprta z dobro kreditno rastjo, visoko kakovostjo portfelja, močnim presežnim kapitalom in privlačno dividendo. Višji Euribor izboljšuje obrestne obete, dodatno zanimanje pa prinaša aktualna prevzemna zgodba okoli Addiko Bank.

Trg dela v evroobmočju ostaja zelo močan: brezposelnost je maja ostala pri rekordno nizkih 6,2 odstotka, število brezposelnih pa se je znižalo na najnižjo raven v skoraj letu in pol.

Nafta je zdrsnila pod 68 dolarjev za sod: večji pretok skozi Hormuško ožino, okrevanje izvoza iz ZAE in Irana, rekordne ruske pošiljke ter napredek v ameriško-iranskih pogovorih povečujejo ponudbo in pritiskajo na cene.

Fed ostaja zavezan znižanju inflacije: predsednik Kevin Warsh je ocenil, da so se inflacijska pričakovanja v zadnjem mesecu umirila, vendar poudaril, da bo centralna banka vztrajala pri ponovni vzpostavitvi cenovne stabilnosti.

V prihodnjem tednu:

Četrtletna poročila: PepsiCo, Delta Air Lines, Levi's.

Makroekonomski kazalci: Evropa – maloprodaja, ZDA – PMI indkesi, FOMC zapisnik.

Gibanje indeksov

Vir: Bloomberg

Slovenski kapitalski trg je dobil pomembno novost. Na Ljubljanski borzi je začel kotirati ILIRIKA SBITOP TR UCITS ETF, prvi domači ETF na vodilne slovenske delnice. Vlagateljem omogoča, da z enim samim nakupom pridobijo izpostavljenost do indeksa SBITOP TR in s tem do najpomembnejših slovenskih borznih družb. ETF kotira pod oznako SLOTR, njegova upravljavska provizija pa znaša 0,60 odstotka letno. Za trgovanje je na voljo prek mobilne aplikacije in trgovalne platforme ILIRIKA ter drugih članov Ljubljanske borze.

Z enim nakupom do slovenskega trga

Za številne vlagatelje je vprašanje, katere slovenske delnice kupiti, zahtevno. Posameznik mora spremljati poslovanje podjetij, ocenjevati njihovo vrednost, določati deleže posameznih naložb in portfelj skozi čas prilagajati. ETF ponuja preprostejšo rešitev. Z nakupom ene delnice sklada vlagatelj pridobi razpršeno izpostavljenost do podjetij, kot so Krka, NLB, Petrol, Telekom Slovenije, Zavarovalnica Triglav, Sava Re, Luka Koper, Salus in Cinkarna Celje. Namesto izbire med posameznimi družbami lahko tako z enim nakupom investira v osrednji del slovenskega delniškega trga. Če je bilo doslej vprašanje, katere slovenske delnice izbrati, domači ETF ponuja preprost odgovor: kupi slovenski trg.

Celotne dividende ostanejo naložene

Pomembna je tudi oznaka TR oziroma Total Return. Celotne dividende, ki jih sklad prejme od podjetij v indeksu, se samodejno reinvestirajo nazaj v portfelj sklada.Vlagatelj dividend ne prejema neposredno na račun, temveč denar ostaja naložen in povečuje vrednost njegove naložbe. To omogoča delovanje obrestno-obrestnega učinka in je na slovenskem trgu posebej pomembno, saj dividende predstavljajo velik del dolgoročnega skupnega donosa.

Rezultati podjetij potrjujejo pomen razpršenosti

Dogajanje v letu 2026 dobro kaže, zakaj je razpršenost koristna tudi na manjšem trgu. NLB je ob dobri kreditni rasti, visoki kakovosti portfelja in močnem presežnem kapitalu ohranila privlačno dividendno zgodbo, dodatno zanimanje pa prinaša aktualna prevzemna tekma za Addiko Bank. Višji Euribor podpira obrestne prihodke, visoka zaposlenost pa kakovost kreditnega portfelja. Krka je kljub neugodnim valutnim učinkom nadaljevala rast osnovnega poslovanja, Telekom Slovenije pa je z rastjo prihodkov, EBITDA in dobička potrdil uspešnost naložb v optiko, omrežje 5G in družbo IPKO. Petrol je pokazal nasprotno plat posamezne naložbe, saj je regulacija cen goriv ob skoku cen energentov močno pritisnila na marže. Triglav in Sava Re sta medtem ohranila stabilno poslovanje, visoko kapitalsko moč in privlačno dividendno zgodbo. Prav različni odzivi teh družb kažejo, da razpršenost ni zgolj teorija. ETF zmanjša odvisnost vlagatelja od rezultata enega podjetja in združi različne poslovne modele v en portfelj.

Naravna izbira za individualne naložbene račune

Domači ETF bi lahko posebno vlogo dobil v okviru individualnih naložbenih računov. Vlagateljem omogoča, da del dolgoročnih prihrankov prek enega preglednega produkta namenijo domačemu kapitalskemu trgu, ne da bi morali sami izbirati in spremljati posamezne delnice. To je lahko posebej zanimivo za varčevalce, ki želijo sodelovati pri rasti slovenskih podjetij, vendar nimajo časa, znanja ali interesa za aktivno upravljanje portfelja. Ker se celotne dividende samodejno reinvestirajo, je produkt primeren predvsem za dolgoročno varčevanje.

Domačemu bo sledil globalni WORLD ETF

ILIRIKA pripravlja tudi globalni WORLD ETF, namenjen razpršeni izpostavljenosti do podjetij iz gospodarsko razvitih držav OECD. Prvi sklad odgovarja na vprašanje, kaj kupiti doma, drugi pa, kako investirati v razviti svet. Skupaj predstavljata preprosto kombinacijo domače in globalne izpostavljenosti. Vlagatelj lahko del premoženja nameni vodilnim slovenskim podjetjem, drugi del pa razprši med podjetja razvitih svetovnih gospodarstev.

Nov korak za Ljubljansko borzo

Prihod prvega domačega ETF je pomemben tudi za razvoj slovenskega kapitalskega trga. Slovenski vlagatelj lahko prvič prek domačega produkta in domačega upravljavca z enim nakupom investira v košarico vodilnih slovenskih delnic. Večje vključevanje prebivalstva v kapitalski trg bi lahko prispevalo k večji likvidnosti Ljubljanske borze, boljši finančni pismenosti in lažjemu dostopu slovenskih podjetij do kapitala. ETF sicer ni brez tveganja. Njegova vrednost se spreminja skupaj s cenami slovenskih delnic, domači trg pa je zaradi svoje velikosti bolj geografsko in sektorsko koncentriran od velikih svetovnih trgov. Kljub temu vlagatelju ponuja preglednejšo razpršitev, kot jo običajno doseže z nakupom ene ali dveh posameznih delnic. Največja prednost sklada SLOTR je zato preprostost: z enim nakupom vlagatelj investira v vodilna slovenska podjetja, celotne prejete dividende pa se samodejno reinvestirajo.

Read more

Spoštovani,

Vljudno vas vabimo na vpis državnih zakladnih menic Republike Slovenije, ki bo potekal v obliki avkcije in sicer v torek, 7.7.2026.

Oddaja naročila za vpis zakladnih menic je možna prek telefona na 01 300 24 61 ali prek e-pošte na narocila@ilirika.si V primeru oddaje naročila prek e-pošte je potrebno izpolniti Obrazec za oddajo naročila ZM (pdf) in ga priložiti kot priponko v sporočilu.

Za izračun cene pri kateri bo dosežena vaša zahtevana donosnost vas vabimo, da si pomagate s spodnjim kalkulatorjem, ki vam poleg izračunane cene pri zahtevanem donosu izpiše tudi vsoto stroškov navedenih spodaj.

KALKULATOR za izračun donosnosti/obrestne mere zakladnih menic

Vnesite podatke

Izberite vrsto izračuna in vnesite zahtevane podatke.

Izračun je informativne narave. Končni stroški in pogoji so odvisni od veljavnih cenikov, datuma poravnave in pogojev posamezne izdaje. Informacija ne predstavlja investicijskega priporočila.

Predvideni stroški za vpis zakladnih menic ob izdaji so naslednji:

Vzdrževanje stanj (ILIRIKA): 0,0008% vrednosti mesečno

Vzdrževanje stanj (KDD): 0,40 EUR + 0,00107% vrednosti mesečno

Strošek poravnave (KDD): 0,037%, min. 5,00 EUR oziroma max. 30,79 EUR

Strošek za uparitev naloga (KDD): 0,25 EUR

Strošek za izplačilo (KDD): 0,31 EUR

Strošek ob izplačilu menice (ILIRIKA): 15,00 EUR

Kaj so zakladne menice?

Zakladne menice so nematerializirani, serijski, imenski prenosljivi vrednostni papirji z dospelostjo tri, šest, dvanajst in osemnajst mesecev. Izdajajo se v apoenih po 1.000 evrov, nominalna vrednost posamezne razpisane emisije pa je odvisna od vsakokratne odločitve izdajatelja.

Zakladne menice so diskontirani vrednostni papirji: ob izdaji vlagatelji vplačajo diskontirani znesek, izdajatelj pa ob zapadlosti izplača nominalni znesek zakladnih menic. Obresti se izračunavajo z uporabo navadnega obrestnega računa, dekurzivnega načina obrestovanja in z upoštevanjem dejanskega števila dni do dospelosti ter 360 dni v letu.

Primarna izdaja zakladnih menic se izvaja na avkcijah. Vlagatelji oziroma primarni vpisniki na avkciji licitirajo prodajno ceno, s katero se odraža nominalna proporcionalna obrestna mera ponudbe. Posamezna avkcija se zapre pri enotni ceni (oziroma obrestni meri), kar pomeni, da so pri tej ceni sprejete ponudbe z višjo ali enako ceno kot enotna cena (v slednjem primeru so ponudbe lahko delno sprejete), ponudbe z nižjo ceno od enotne cene pa niso sprejete. Imetniki zakladnih menic so lahko tako pravne kot fizične osebe, ki podajajo naročila za vpis pri primarnih vpisnikih za zakladne menice. Poravnava zakladnih menic se izvede dva delovna dneva po avkciji.

Zakladne menice so uvrščene med instrumente denarnega trga Ljubljanske borze.

V kolikor bi želeli izvedeti več o podrobnostih in lastnostih zakladnih menic si lahko preberete Ponudbeni dokument za izdajo zakladnih menic.

Donosnost menic je odvisna predvsem od tržnih razmer na trgu dolžniškega kapitala. Dejanska donosnost za posamezno menico pa se oblikuje na podlagi enotne prodajne cene, določene na avkciji. Za lažjo predstavo o višini letnega donosa si lahko ogledate podatke o zadnji sprejeti donosnosti zakladnih menic glede na obdobje zapadlosti:

Trimesečne zakladne menice (Oznaka: TZ231): 2,20 %

Šestmesečne zakladne menice (Oznaka: SZ161): 2,48 %

Dvanajstmesečne zakladne menice (Oznaka: DZ123): 2,68 %

Osemnajstmesečne zakladne menice (Oznaka: OZ24): 2,68 %

Vabimo vas, da stopite v stik z nami in pridobite več informacij. Naša ekipa borznih posrednikov vam nudi celovito podporo pri nakupu in prodaji vrednostnih papirjev. Za vsa vaša vprašanja in zanimanja smo dosegljivi na naslednjih kontaktnih podatkih:

E-pošta: trgovanje@ilirika.si

Telefon: 01 300 24 61

Read more