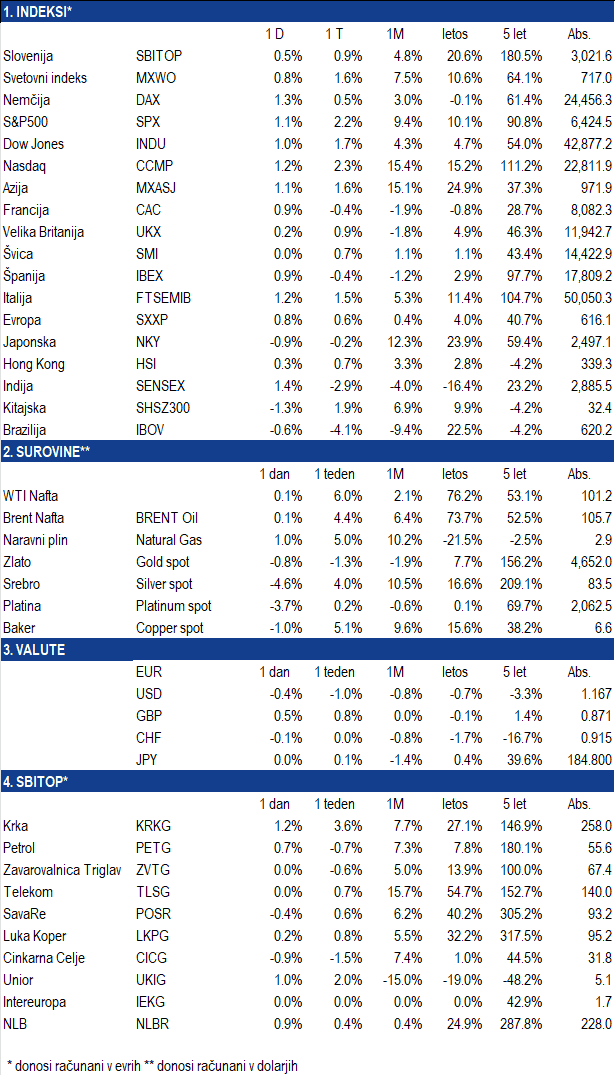

Krka demonstrated exceptional performance in the first quarter. Revenues reached 565.8 million euros, represents an 8 percent increase compared to last year, EBITDA was 175.7 million euros (+20 percent), and EBIT stood at 151.6 million euros (+24 percent). The EBITDA margin rose to 31.0 percent. The 21 percent decline in net profit is primarily a consequence of a high comparative base, as last year's first quarter included 57 million euros in one-off positive effects due to the rouble. The Russian market remains very strong, with revenues growing there by 28 percent to 122 million euros, and local production at Krka-Rus already covers 72 percent of local demand. The company is proposing a record gross dividend of 9.10 euros per share and the expansion of the share buyback programme to up to 10 percent of the share capital with the option of cancellation.

Telekom Slovenije published stable results. Revenues amounted to 178.7 million euros (+4 percent), EBITDA was 66.0 million euros (+7 percent), and net profit reached 16.0 million euros (+12 percent). The EBITDA margin reached a high of 36.9 percent. The number of mobile users exceeded two million for the first time, while the number of fixed lines increased to 322,372. The management board maintains its targets for 2026, whilst once again drawing attention to the regulatory burden, as Telekom is the only operator still regulated in the field of fixed broadband access, despite holding less than a 29 percent share in this market.

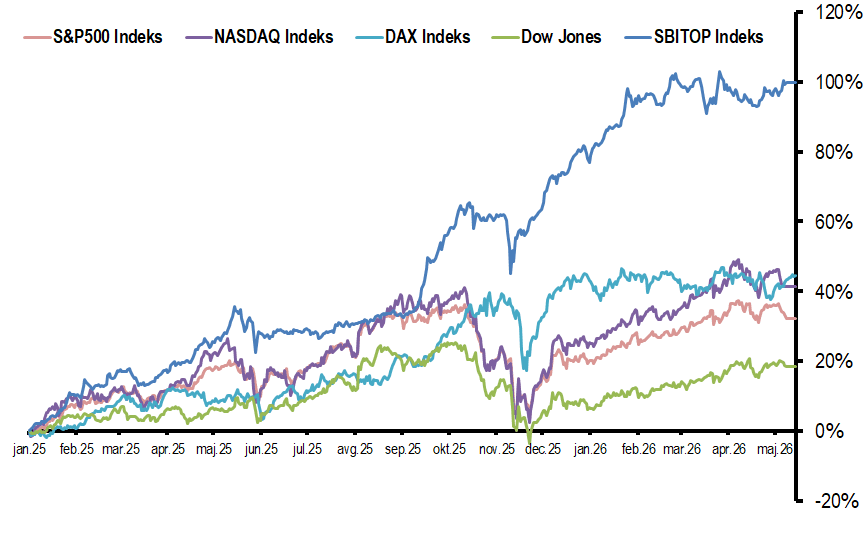

SBITOP – the index crossed the 3,000-point threshold on 13 May, closing at 3,007.53. It has gained approximately 17% since the beginning of the year, with trading once again driven primarily by NLB shares.

USA: inflation – April CPI hit 3.8% annually, while PPI surprised with 1.4% monthly and 6.0% annual growth. Since pressure is also coming from services, markets are increasingly writing off a rapid cut in interest rates.

USA: retail sales – April spending appeared strong at first glance, but was partly due to one-off higher tax refunds. Against a backdrop of weaker sentiment & a low savings rate, a slowdown in discretionary spending is likely in the remainder of the quarter.

Slovenian labour market – unemployment remains low, with 44,175 people out of work in April, representing 0.4% less than in March and a year ago. The fly in the ointment remains the rise in youth unemployment, which is 4.7% higher year-on-year.

AI infrastructure – in the US, more and more local communities are restricting the construction of large data centres. Electricity, water, and local approvals are becoming a significant bottleneck for the continued expansion of artificial intelligence.

In the coming week:

Quarterly reports: Nvidia, Walmart, Home Depot, John Deere, Analog Devices, Richemont, Rose Stores, Target.

Macroeconomic indicators: Europe - PMI index, labour market data; USA - PMI indices.

Index movements

Source: Bloomberg

This week turned around a narrative that seemed almost self-evident just a month ago. The expectation that US inflation was gradually closing in on its target and that the Fed would start cutting interest rates in the second half of the year ran headfirst into an unfavorable series of data. First, the April CPI showed 3.8% annual growth, which was followed by an exceptionally hot PPI: 1.4% monthly and 6.0% annual growth, the highest since the end of 2022.

It is difficult to speak of a mere energy shock. It is true that wholesale petrol prices jumped by more than 15%, with the link to tensions around the Strait of Hormuz being obvious. However, a much more significant signal comes from the core part of the data. Core PPI, excluding food, energy, and trade services, rose by 0.6% m/m or 4.4% annually. The service sector contributed nearly 60% of the total monthly increase, representing the largest shift in services pricing in the last four years. Inflationary pressure is therefore spreading from energy into the broader corporate input cost structure, and this is happening much faster than could be explained simply by higher oil prices.

The ramifications for market expectations were immediate. As recently as the start of the week, the interest rate derivatives market pointed to the possibility of two rate cuts by the end of the year. Following the PPI release, this scenario was virtually wiped off the table, and the possibility of further Fed policy tightening started to be priced in once again. This represents a significant shift for portfolios that had been positioned on the assumption of gradually falling yields.

In the background, a political dimension is also intertwined. Jerome Powell's mandate expires today, and the expected successor Kevin Warsh is considered more dovish on interest rates and much more open to political pressure from the White House. Markets are thus entering a period where macroeconomic data is pushing in one direction, while the potential new central bank leadership is leaning in another. It is precisely this gap that will be key to the Fed's credibility in the coming months, and consequently for the path of the dollar and long-term US bond yields. The yield on the 10-year US Treasury briefly surpassed 4.49% mid-week, hovering just below the psychologically important 4.5% threshold.

The most misleading figure was April retail sales. At first glance, it appeared robust, with core retail sales growing at their fastest pace since mid-2022 over the final three months. However, two temporary factors lie behind this: higher tax refunds and very warm weather in March, which pulled forward some consumer spending.

Both of these effects are now fading. Tax refunds are decreasing in May, and the weather impact is normalising. At the same time, real incomes are falling, consumer confidence remains low, credit card spending is losing momentum, and the savings rate is already below the long-term average. Consequently, the second half of the second quarter is likely to bring more pressure on discretionary spending, arriving just as the Fed and markets will be assessing new inflation data.

The empirical picture remains split. Inflation data is nudging the Fed towards higher interest rates or keeping a restrictive policy in place for longer, whereas poorer sentiment and the anticipated cooling of consumer spending indicate that economic activity could begin to slow down more rapidly. This clash between inflationary pressure and weaker consumption will be critical over the next two to three months, coinciding precisely with the transition of leadership at the helm of the US central bank.

There are two takeaways for European investors. Firstly, the ECB could also find itself facing a similar dilemma with a lag of a few months, as higher energy prices place upward pressure on European inflation too. Secondly, European markets are losing a key support pillar of recent months: the expectation that the Fed would support global liquidity by lowering interest rates.

This is particularly relevant for dividend stocks and banks in the CSEE region. If interest rates remain higher for longer, expectations of lower net interest margins and cheaper funding for acquisitions will shift. For the Slovenian market, this translates to a relative advantage for companies with a net cash position, stable margins, and less sensitivity to higher capital costs.

Krka as a high-quality pillar of the Slovenian market

With its first-quarter results for 2026, Krka has once again demonstrated why it is regarded as one of the highest quality companies on the Slovenian market. Revenues grew by 8%, whilst operating profit rose even faster, indicating that the company is not only growing in scale but is also operating with increasing efficiency.

Importantly, this growth is not dependent on a single market. Krka increased its sales across most regions, from Eastern and South-Eastern Europe to overseas markets. This shows that it possesses a stable and well-diversified business model.

Much attention remains focused on Russia, where sales grew by 28%. However, it is vital to note that Krka already manufactures most of its products locally there, making it less vulnerable to supply chain disruptions or political risks than many of its competitors.

Further confidence is provided by the company's plan regarding share buybacks. Through this, the management is signalling that it believes in the long-term value of the company and considers the stock to still be attractive.

At first glance, the 21% drop in net profit might be concerning, but the reason is primarily accounting-related. Last year, Krka benefited from a one-off positive effect due to rouble fluctuations, so the comparison is not entirely realistic. If this effect is stripped out, underlying profit is actually growing this year.

Today, Krka combines several features that investors highly value in an uncertain environment: stable growth, a strong cash balance, a regular dividend, and zero debt. It is for this reason that the company remains one of the key pillars of the Slovenian capital market. In this context, the SBITOP index breaking past the 3,000-point mark increasingly seems less like an anomaly and more like a logical consequence of the relative appeal of the Slovenian market in an environment of heightened global uncertainty.